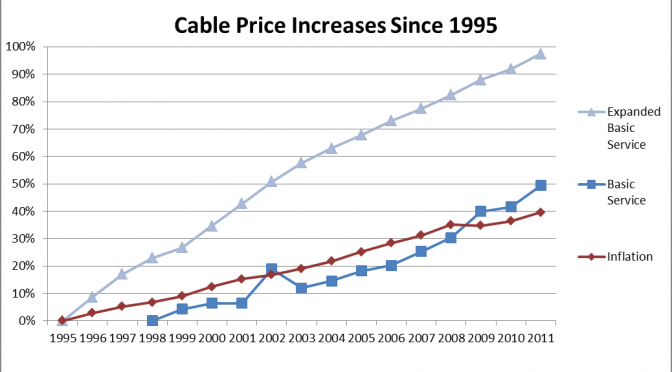

Assembling big (often 50+ channels) bundles of cable networks has been the primary strategy of multichannel video service providers (cable, DBS, telco cable, etc.) for the last couple of decades. Keeping bundles big helps minimize transaction costs for the bundler, while offering maximal potential audience reach for advertisers, and maximizing the viewer's ability to browse and discover the value of channels and their content. On the other hand, critics complain that it "forces consumers to purchase channels they aren't interested in." That's not necessarily true, as purchase decisions are based on the aggregate perceived value of the bundle, not the "costs" of undesired channels (see here for more detailed analysis).

However irrelevant, the claim of paying for unwanted channels is a major theme for those who would prefer to force multichannel services to unbundle channels and offer them to consumers in small focused bundles (like the various Discovery channels), or individually (i.e. "a la carte"). This may seem to be a good deal for consumers - until you realize that going a la carte will, in most cases, reduce audience reach numbers significantly. One study (discussed here) forecast that forced unbundling could result in a loss of 60% of advertising revenues for cable networks, and result in more than 100 channels going out of business. And since cable networks would need to significantly increase their a la carte prices to recapture some of those losses, going a la carte would also likely result in higher total costs for cable network access for most consumers.

Meanwhile, some multichannel video providers are finding that the increased licensing demands made by some networks are crossing that value threshold, and are dropping channels, or in one case offering to provide the channel - but only as an a la carte service. The networks have so far been smart enough to realize that either option is a net loss for them, but the gleam of a licensing El Dorado of unlimited wealth keeps them trying to push licensing fees ever higher. Viacom, and its package of networks, is the latest battleground, with their channels being dropped by a number of mid-range and smaller cable systems unwilling to cave into their licensing demands. As one analyst noted,

“The stage is set... As consumers are less interested in large bundles, somebody is going to get hurt in the process by asking for too much.”If multichannel service providers remained the only option for access, the impact on the industry would be bad enough. However, they're facing rapid growth in the ability of broadband internet connections to provide access to high-quality TV streams to mobile devices and wired connected devices. The term OTT (over-the-top) refers to these alternative sources of video and TV content. Both the diffusion and use of these technologies for TV viewing are growing rapidly (see here and here). Combined with increased time-shifting of programs and place-shifting, audience TV viewing habits are clearly changing. For cable networks, going online for their content distribution - either as single channels or as a part of a more limited (and much less expensive) bundle offered online - is an increasingly viable supplement, and potential substitute, for traditional delivery media.

The viability of online TV delivery has been a significant component of the "TV Everywhere" marketing push. The initial conceptualization, though, saw "TV Everywhere" as a way of achieving multichannel services beyond the household's TV sets - and not as a substitute or replacement for those services. That was one reason for the rapid reaction to the Aereo service. One would think that local stations and networks would be eager to extend their range of service via mobile as a way of enhancing (or at least maintaining) audience reach. However, it seemed that the industry hated the notion of a video service that paid no licensing fees; and the courts bought that argument.

In addition, CBS has been offering an online video service since last fall, and it is thought that ABC, NBC, and ESPN are considering taking their online video channels public (currently access is limited to subscribers of some of the largest multichannel providers). Most cable networks provide some access to their content, but not to live streams of the channel.

Still, it's likely that the new DishTV service, Sling-TV, may unleash the deluge. Sling-TV is an OTT service that bundles a number of the most popular cable networks as a minibundle at a very low subscription price ($20/mo. for about 20 channels), and supplements that with targeted minibundles (sports, movies, children, etc.) at $5 a pop. The service combines live streams of the network, as well as on-demand access to the previous week's programs. Sling-TV has managed to sign up some 100,000 subscribers in its first month, despite being initially limited to those with a Roku OTT box.

The Sling-TV service could well force the big multichannel services to start unbundling. It offers an intriguing alternative for those who would be satisfied with a lesser selection of channels. And even for those viewers who place high value on channels not included in the Sling TV packages, the price contrast between the "big bundle" options ($50-$150+ on new subscriber deals) and Sling-TV will prompt consumers to reconsider if their demand for favorite channels will justify the price differential (and to wonder how the costs of channels they don't want inflate bundle prices).

The big multichannel providers have been shedding TV subscribers slowly, but consistently, for years. Now that viable and less costly OTT and online video options are coming available, expect the decline in pay TV subscribers to increase, particularly for major MSOs and multichannel providers.

Sources - Updating: HBO Now The Big Test for Cord Cutters?, Online Video Daily VidBlog

Sling TV notches 100,000 users in a month, TechHive

Seventeen percent of U.S. broadband households are likely to subscribe to an OTT HBO service, Parks Associates report.

Provider's Dispute with Viacom Highlights Skirmish Over the Cable Bundle, New York Times

No comments:

Post a Comment